The past five years for easyJet (LON:EZJ) investors has not been profitable

Statistically speaking, long term investing is a profitable endeavour. But unfortunately, some companies simply don't succeed. For example, after five long years the easyJet plc (LON:EZJ) share price is a whole 65% lower. That's an unpleasant experience for long term holders. The falls have accelerated recently, with the share price down 16% in the last three months.

So let's have a look and see if the longer term performance of the company has been in line with the underlying business' progress.

View our latest analysis for easyJet

Because easyJet made a loss in the last twelve months, we think the market is probably more focussed on revenue and revenue growth, at least for now. Shareholders of unprofitable companies usually expect strong revenue growth. That's because it's hard to be confident a company will be sustainable if revenue growth is negligible, and it never makes a profit.

In the last five years easyJet saw its revenue shrink by 9.3% per year. That's definitely a weaker result than most pre-profit companies report. Arguably, the market has responded appropriately to this business performance by sending the share price down 11% (annualized) in the same time period. We don't generally like to own companies that lose money and don't grow revenues. You might be better off spending your money on a leisure activity. You'd want to research this company pretty thoroughly before buying, it looks a bit too risky for us.

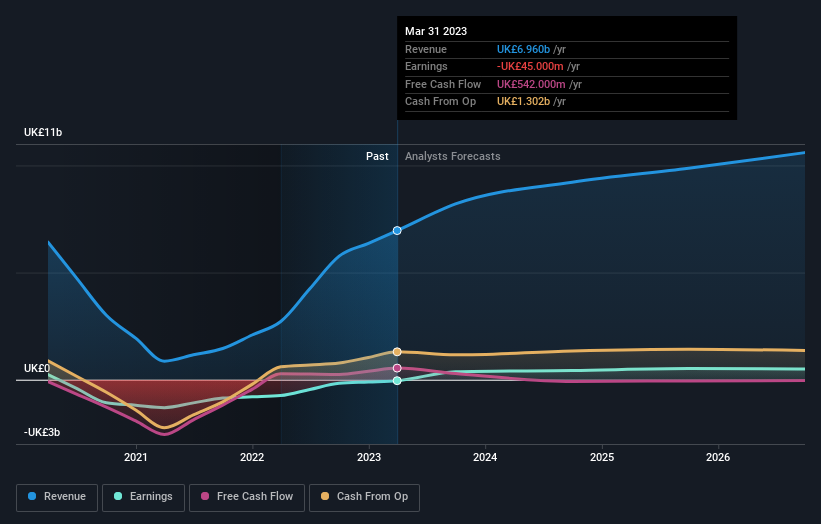

You can see how earnings and revenue have changed over time in the image below (click on the chart to see the exact values).

easyJet is a well known stock, with plenty of analyst coverage, suggesting some visibility into future growth. You can see what analysts are predicting for easyJet in this interactive graph of future profit estimates.

What About The Total Shareholder Return (TSR)?

We've already covered easyJet's share price action, but we should also mention its total shareholder return (TSR). The TSR is a return calculation that accounts for the value of cash dividends (assuming that any dividend received was reinvested) and the calculated value of any discounted capital raisings and spin-offs. Its history of dividend payouts mean that easyJet's TSR, which was a 55% drop over the last 5 years, was not as bad as the share price return.

A Different Perspective

We're pleased to report that easyJet shareholders have received a total shareholder return of 40% over one year. That certainly beats the loss of about 9% per year over the last half decade. We generally put more weight on the long term performance over the short term, but the recent improvement could hint at a (positive) inflection point within the business. If you would like to research easyJet in more detail then you might want to take a look at whether insiders have been buying or selling shares in the company.

Of course easyJet may not be the best stock to buy. So you may wish to see this free collection of growth stocks.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on British exchanges.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.